Danaher's actions are under pressure on Wednesday, since the profit results of the fourth quarter of the Holding Club reached mixed and a disappointed orientation. The company known for its operational excellence is even more testing our patience. The income for the three months ended on December 31 advanced 2% year after year, to $ 6.54 billion, exceeding the Estimate of LSE consensus of $ 6,43 billion. On an organic basis, sales increased by 1% compared to the period of the previous year. The profits adjusted by Action (EPS) increased 2.4% per year, to $ 2.14, but fell short compared to the estimate of consensus of $ 2.16, showed the LSEG data. It is the first time that Danaher was lost the quarterly consensus of the EPS from at least the fourth quarter of 2019, according to Factset. The shares fell more than 8%, at approximately $ 226 each, in the afternoon negotiation on Wednesday. Losses have dragged the stock to a negative territory year to date. Danaher entered the session approximately 8% so far in 2025, part of a strong start of the year for the healthier health sector. DHR 1 and Mountay Danaher's stock performance in the last 12 months. In a nutshell, another disappointing launch of Danaher, which extends a streak of inconsistent results in the last two years, does not leave us with no other option to reconsider this position. On Tuesday, we cut 50 shares and degrade the name to a rating of 2 discipline equivalents. He arrived when the actions obtained a thorough impulse of the results of the European pairs Sartorius. Of course, in retrospect, we should have sold more. That is not easy to admit for how very much we have thought of this company and its management in the past. And we are not just us: Danaher's corporate strategy to boost growth and make shareholders, Danaher's commercial system, call the subject of Case studies of Harvard Business School. Danaher provides products and services to multiple corners of the health industry, including those used in the discovery and production of medicines, as well as the diagnostic tools found in hospitals and doctors offices. Its clients also include academic research laboratories and pharmaceutical and biotechnology companies. We do not reach our dissatisfaction in a hurry. During the monthly meeting of January, we highlight our disappointment due to the lack of growth of China. While the slow Chinese economy cannot be blamed for management, the lack of management of investors can. By aggravating our existing frustration, management sounded so optimistic on Wednesday despite what we see in real results and formal orientation. The credibility of the team has once again doubted. For now, we are lowering our objective price in the shares to $ 270 per share of $ 305, which reflects the growth now lower than expected now predicted by 2025. In fact, the true driver of disappointment on Wednesday is the perspective of Danaher for the current quarter and complete fiscal year. The Management had prevailed these decidedly mixed results of the fourth quarter earlier this month, in the influential JPMorgan Health Conference, which joined the anticipation of Wednesday's guide. What we obtained was not good enough, with the growth of the expected basic income for both periods below the Wall Street consensus. Danaher Why we possess it: Danaher is the best company of life sciences and diagnosis of the class linked to secular growth trends as a global population that ages, a change in medicine to biologicals and the emergence of monoclonal antibodies, Among other issues. In recent years, Danaher has restructured its portfolio towards faster and greater margin opportunities within medical care. But it has been a trip full of potholes, with Danaher struggling to return to sustainable growth because customers work on the excess inventory of the Covid era. Our investments recognize continuous winds with long -term potential. Competitors: Sartorius and Thermo Fisher Scientific Weight in Portfolio: 3.27% Purchase more recent: November 18, 2024 Initiated: January 3, 2022 between the few bright points in the fourth quarter: the free cash flow reached $ 1.5 billion , which represents almost 30% growth versus the period of the previous year. The company also achieved a free cash flow relationship to net income of 138%. For the whole year, that relationship reached 136%. Anything above 100% means that the profits of a company are fully backed by cash, a sign of high quality profits. Danaher cleared that bar, and something else. In addition, during the fourth quarter and in January, Danaher recovered around 8 million shares, totaling around $ 1.9 billion. The quarterly comments of Danaher's salts in the developed markets were approximately in the quarter, since a low -digit decrease in North America was compensated by a low digit increase in Western Europe. High growth markets increased a single digit, since the impulse outside China more than compensated a single digit decrease in China. Basic biotechnology revenues increased 8% year after year, with orders that increase the high digit points sequentially. In general, basic income eliminates the impact of foreign exchange fluctuations, as well as mergers and acquisitions. It helps to soften comparisons year after year and better capture how the segment is being worked. The book at the Biotechnology segment bill was approximately 1. Anything above 1 indicates that more orders were received than completed in a certain period. The adjusted operational benefit margin was 38.6%, more than 200 basic points year after year. A basic point is equal to 0.01%. Bioprocessing sales increased high digit points, and gradual recovery is observed throughout the year continuing in the fourth quarter. In China's key market, management said that “the activity levels were relatively stable”, but in general they remain weak due to a difficult financing environment. The central income of Life Sciences increased by 1% year after year. The adjusted operational benefit margin of the segment expanded 320 basic points year after year, to 25.8% of instrument sales increased slightly, exceeding management expectations in the United States and Europe. In China, CEO Rainer Blair said Danaher observed “modest demand improvements” during the quarter. “While we saw a modest benefit of the ongoing stimulus program, market conditions continue to be challenging as customers remain cautious with their investments,” he said. Basic diagnostic income decreased by 2% year after year. The adjusted operating profit margin contracted 170 basic points compared to the period of the previous year, 29.2% of clinical diagnostic companies realized a fundamental income growth combined in the low -sole digit rank, directed by Leica Biosystems, where sales increased almost 10% of the year. With the year. Cepheid's respiratory sales reached $ 550 million, far ahead of the approximately $ 350 million expected by the administration, due to the increase in volumes and a favorable sales combination of the four-in-one of Danaher for Covid-19, The flu A, flu B and the respiratory. Syncitial virus, or RSV. Orientation for current quarter, Danaher expects central income to decrease in low digits compared to last year, missing the expectations of an increase of 2.9%, according to estimates compiled by FACTSET. Danaher's adjusted operational benefit margin is expected to be approximately 26.5%, below 30% of the street. Biotechnology revenues are expected to increase from 6% to 7%, while basic income is expected for life and diagnostic science segments to decrease the percentage points of a single digit. Throughout the year, management predicts basic income growth of 3%, also a failures versus expectations for an increase of approximately 5%, according to Factset. The adjusted operational benefit margin is expected to be approximately 28.5%, below the Wall Street consensus of 29.7%. It is expected that the growth of the basic income of biotechnology will be between 6% and 7%, the expectations of the FISS versus analysts for an increase of 8% year after year, according to FACTSET. It is projected that the growth of the central income of Life Sciences will increase the percentage points of low digit. That is compared to the Wall Street consensus of the annual growth of 4%. The growth of the central diagnostic income is expected to be in the range of percentage points of low -digit floor. That is compared to an annual growth estimate of a single digit. (Jim Cramer's charitable trust is long DHR. See here a complete list of actions). As a subscriber of the CNBC Investing Club with Jim Cramer, he will receive a commercial alert before Jim makes an exchange. Jim waits 45 minutes after sending a commercial alert before buying or selling an action in the portfolio of his charitable trust. If Jim has talked about an action on CNBC TV, wait 72 hours after issuing the trade alert before executing the operation. The information of the previous investment club is subject to our terms and conditions and privacy policy, together with our discharge of responsibility. There is no fiduciary obligation or duty, or is created, by virtue of receiving any information provided in relation to the investment club. No specific results or profits are guaranteed.

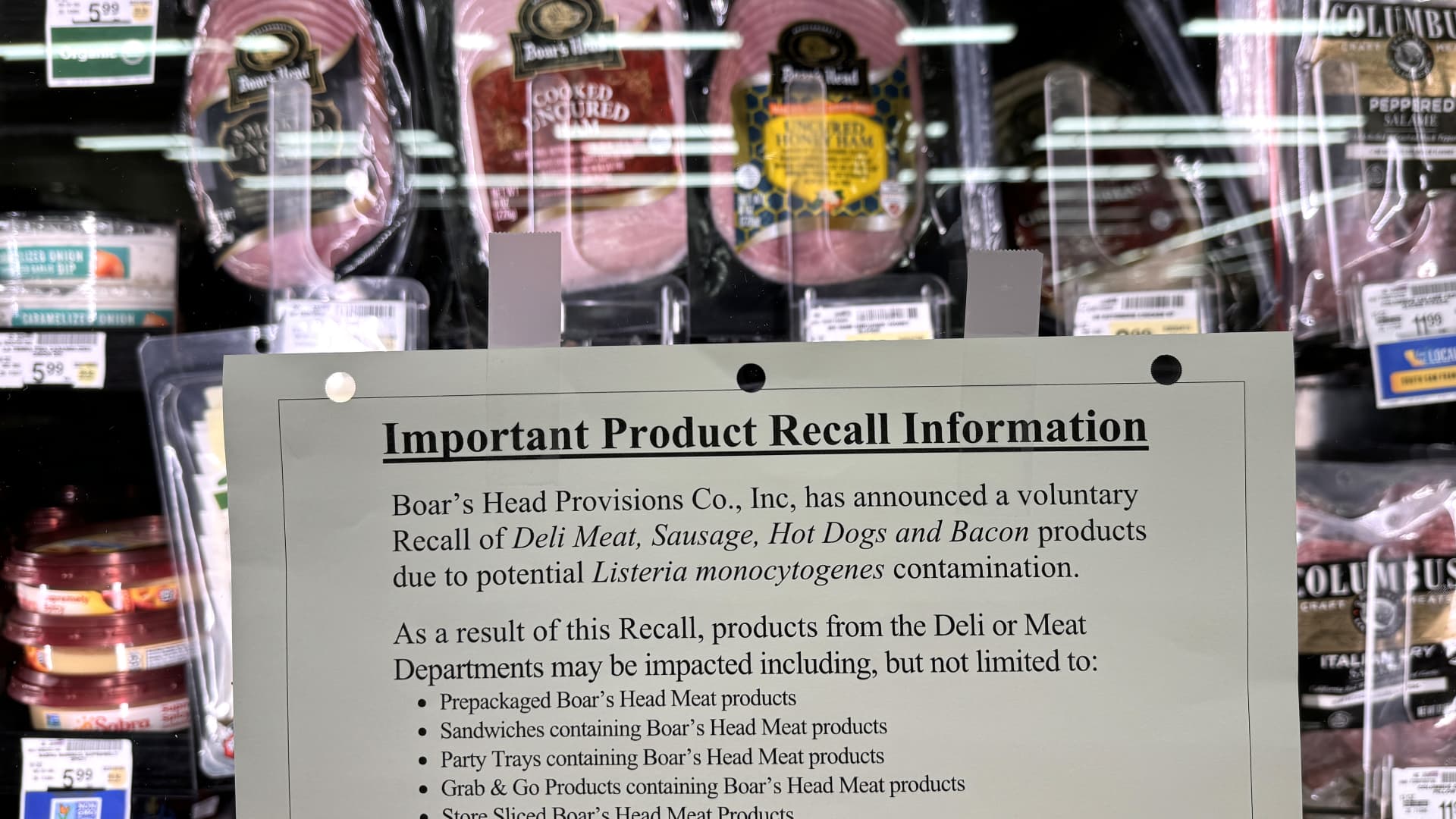

A worker uses a machine made by Pall Corp. during a demonstration of the clarification stage of the production of influenza vaccine during a tour in a vaccine production installation of Sanofi Pasteur vaccines on Swiftwater, Pennsylvania.

Stephen Hilger | Bloomberg | Getty images

Danaher The actions are under pressure on Wednesday when the results of the fourth quarter of the Holding Club arrived mixed and the disappointed orientation. The company known for its operational excellence is even more testing our patience.